Market Ethos

29 June 2026

Dollar drama

Sign up here to receive the Market Ethos by email.

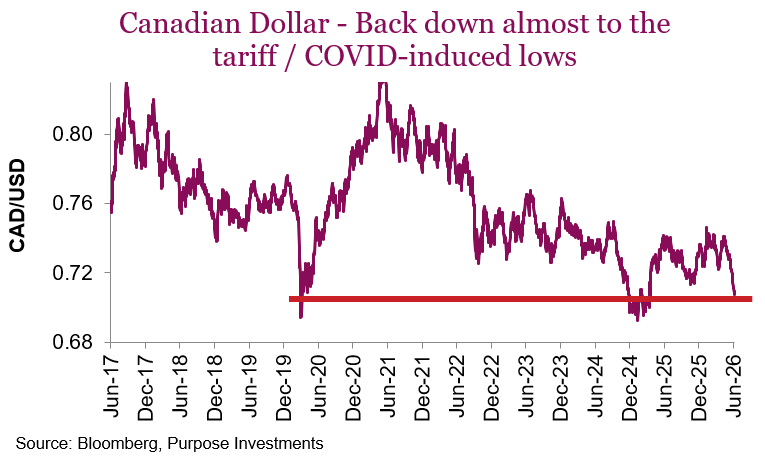

Big moves are becoming the norm in this market and currency is no exception. Our Canadian Dollar (CAD) has traded down to 70 cents on the dollar. This is only a penny or two away from the extreme lows of COVID (when everyone was hiding in USD/Treasuries) and Tariff Day (remember when tariffs were going to push Canada into a bone-crushing recession). Too extreme? Let’s bring it in.

Our initial thoughts on this weakness were that it was a Canada problem. Oil prices have come down from $92 to $70/bbl over the past month, and we are still somewhat of a petro currency. Gold has fallen from $4,500 to just below $4,000/oz; are we a bit of a gold currency now too? Two-year government yields in Canada have fallen a bit from 2.85 to 2.75%, while U.S. Treasury 2-year yields have risen from 4.03 to 4.16%. Canada just printed two quarterly GDP contractions, being labelled a ‘technical’ recession’. It isn’t really a recession but positive GDP in the U.S. is clearly better than anything with a negative sign in front of it.

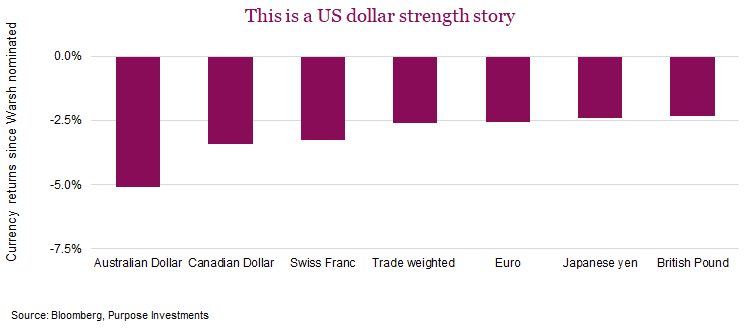

Going through that list, should we not expect a lame duck loonie? But it’s not us, it’s them. ‘Them’ in this case is U.S. dollar strength, not Canadian dollar weakness. The Japanese yen has pushed back up to 162 (up is down for the yen), the lowest value for yen vs the US dollar dating back to the early 80s. Not as epic, the euro has recently weakened as well. In fact, since the new Federal Reserve Chair Kevin Warsh was confirmed, the U.S. dollar has been on a tear upwards against just about everyone.

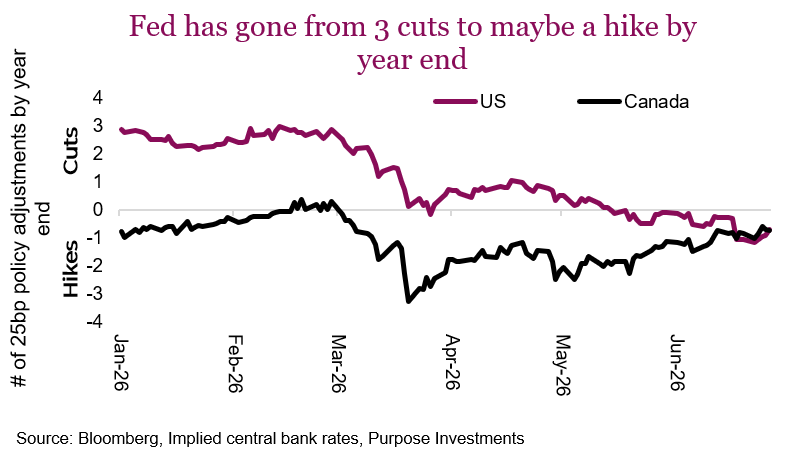

Last year (and during the first couple months of 2026), there was a mild debasement trade focused on the U.S. dollar. Erosion of trust in leadership and policy such as tariffs did not sit well. Neither did deficits continuing to run at recession levels despite the overall U.S. economy doing well. But perhaps the biggest concern was about the transition of the Federal Reserve Chair. President Trump’s vocalized desire for lower interest rates and other actions raised concerns over Fed independence. The good news: Warsh has a reputation for being a bit of an inflation hawk and given early statements emphasizing price stability, Fed independence fears have faded for now.

Add an uptick in inflation data, partially caused by the energy impact from the temporary blockage of the Strait of Hormuz, but not just this factor. The economy is strong, employment has picked up as well, and the data sure doesn’t support cutting. Given the new Fed chair and the market’s view of more data-dependent decision making, expectations for rate cuts have dissipated. The futures market was expecting the Fed to cut three times in 2026 (bad for its currency) but now pricing in no change or even one 25 bps hike. Expectations for the Bank of Canada have largely remained in the “no change” camp.

As a result, including many other factors as well, we have seen a widening of short-term yield spreads. Two-year yields are 4.07% in the U.S. and 2.75% in Canada, and as that spread widens the CAD drops vs USD. At the beginning of May the spread was 1.0%, now we are 1.32% after touching 1.40%. This is pretty extreme spread territory, which should be somewhat supportive for CAD.

The stronger U.S. dollar is not just a currency story. It is impacting everything from gold, crypto and global equity markets.

Where to go from here?

In the short term, we are at pretty extreme levels of the CAD/USD exchange rate and yield spreads. And the sudden optimism around U.S. Fed independence could prove to be short-lived. A couple of economic data prints that you-know-who doesn’t like and he could very well crank up the pressure on the Fed to cut rates. This does have us in the camp that things have gone too far the other way, from USD weakness to USD strength. At 70 cents, we are certainly starting to think about hedging USD currency a bit more.

We are becoming somewhat more constructive on gold too. For much of the past year, gold prices were largely influenced by money flows into (or out of) ETFs. Currency, real yields, and geopolitical risk, commonly drivers of gold, had taken a back seat to flows. In 2025 that was a good news story; in the first half of 2026 clearly not. But over the past couple weeks, gold is starting to behave based on fundamentals again. This may imply gold has reinstituted its defensive characteristics.

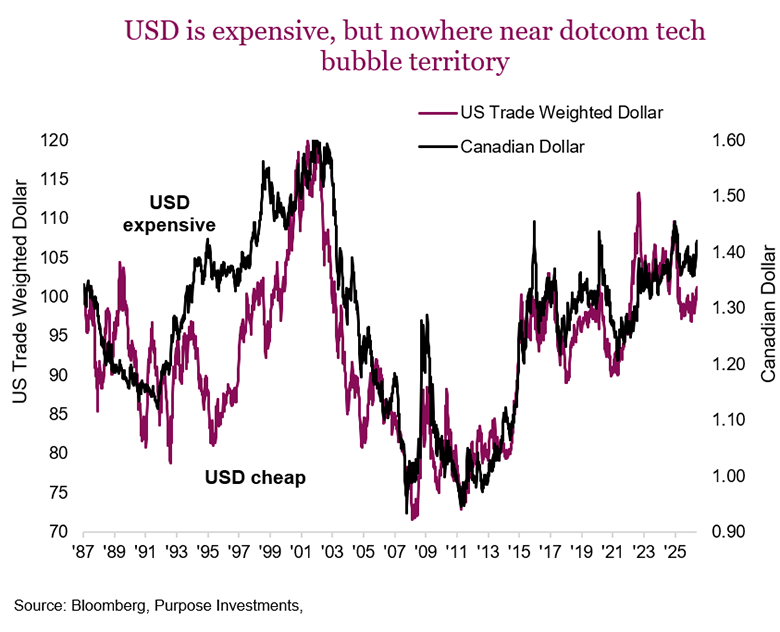

For the CAD/USD exchange rate, one caveat is AI. Investors may be hard pressed to remember, but during the last tech bubble in the late 1990s, the U.S. dollar flew with the CAD down to 65-cent levels. There were a number of different tailwinds, with the tech bubble being a big one as more and more capital flowed into America. This AI bubble is more geographically broad, but still with significant U.S. leadership. A continuation could result in more U.S. dollar strength. Conversely, any hiccup and we would expect to see USD weakness.

Final thoughts

Forecasting currencies? Good luck. That being said, it is a zero-sum game in the really long term and sometimes factors all align in one direction. We think this encapsulates the past few months. After a year of mild USD weakness, most factors became USD bullish (CAD bearish). Oil, relative economic growth, inflation, yields and the market’s best guess on central bank future behaviour. In our view, the only time forecasting currencies becomes a bit easier is when everyone is on one side of the boat. That feels like today.

At 70 cents, it’s probably a good time to consider some hedging of U.S.-denominated assets.