Sign up here to receive the Market Ethos by email.

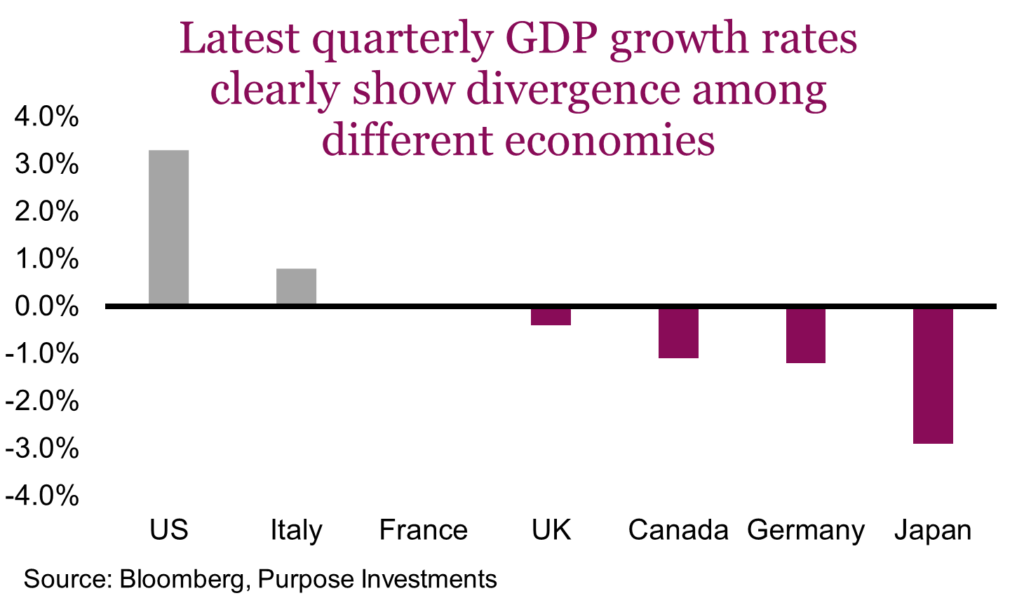

Over the past month or so, the economic data from America has certainly turned up somewhat. A strong Q4 GDP print of 3.1%, two back- to-back months of 300k+ job gains, even manufacturing activity has ticked higher. So where is this recession that has been the talk of the town for the past year or even longer? It appears to be most everywhere else. Maybe not outright recession, but certainly weakness. The latest GDP readings are negative in UK, Canada, Germany and Japan, leaving only two of the G7 members with positive economic growth.

Much of this divergence can be explained by two factors: economic sensitivity to interest rates and global trade. Countries that are more sensitive to rates and global trade are doing worse, those less exposed are doing better.

As we all know, rates/yields have moved higher substantially over the past couple years, yet that impacts different parts of the economy differently. And based on different economic compositions from one country to the next, rate changes can hurt more or less. The U.S. for instance, is less sensitive to rates given the structure of their mortgage market. Dominated by 30-year fixed mortgages, changes in rates don’t impact consumers’ mortgage payments as much. It is estimated the U.S. has less than 10% of mortgage set to variable rates; compare that with 30% in Canada. Furthermore, fixed mortgages in Canada max out at five years, meaning the resetting of payments higher is increasingly being felt as mortgages are renewed.

GDP = C + I + G + (X -M)

C = consumer spending I = investment

G = government spending X-M = exports minus imports or trade.

Different countries have different weights in these categories. For instance, consumer spending is by far the biggest piece of the U.S. economy while trade is relatively small. Compare that to Germany or Japan, both of which have much larger economic weightings in trade. Same with Canada.

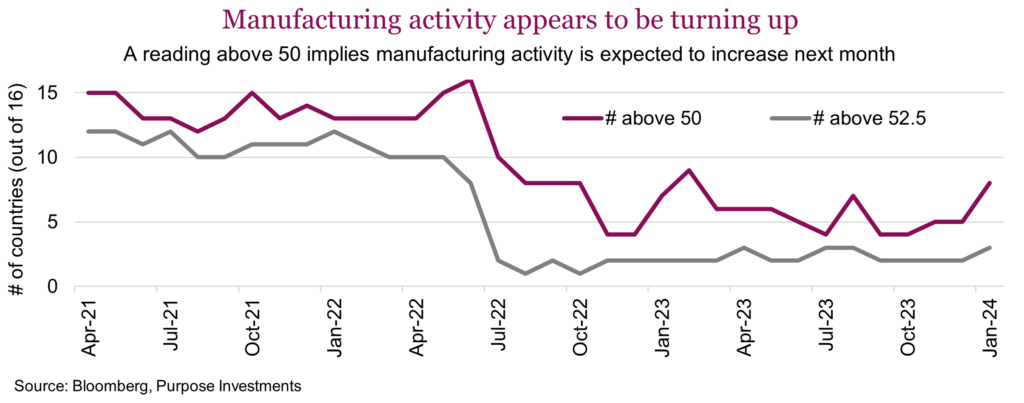

The big question is whether or not U.S. economic exceptionalism can endure long enough to wait for negative economic momentum elsewhere to turn the corner. Afterall, even if an economy is less sensitive to higher rates or slowing global trade, it still has an impact. There is some encouraging news on the global trade front. While still early, Purchasing Manager surveys that provide a proxy for manufacturing activity have started to improve. Half of the 16 biggest manufacturing countries had a PMI reading in January above 50.

While encouraged, our view on manufacturing is tempered. Manufacturing activity exploded during the pandemic as we all wanted more goods. As the pandemic diminished, consumers returned to more normal spending patterns. So that spike in 2021/22 was followed by a dearth in 2023. Global spending growth does appear to be slowing, likely a result of higher rates.

Wait for it, but we could be getting close to a period when good economic news stops being good for markets. This incredible run over the past three months that has seen the S&P 500 rise 14 of the past 15 weeks, a feat not repeated since the early 1970s. The initial rise was from an oversold market that started celebrating more evidence that inflation was coming down, opening the door for rate cuts this year. This changed from inflation optimism to optimism about U.S. economic strength. Unfortunately, strong economic growth does not jive with rate cuts nor with inflation making a speedy decline down to the magic 2% realm.

Final thoughts

The U.S. is the biggest economy in the world and its equity market now carries about a 70% weight in the MSCI World Index. Yes, if you buy a passive cap weighted global equity ETF, it’s really just the S&P 500 plus some odds and sods. The U.S. economy could certainly remain immune to slowing growth elsewhere. Maybe the stock market can keep climbing with earnings growth slowing. However, the biggest constant for both markets and economies, is often reversion to the mean. And both are well above their means at the moment.

Sign up here to receive the Market Ethos by email.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Craig Basinger, Chief Market Strategist at Purpose Investments Inc. Effective September 1, 2021, Craig Basinger has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Related articles

Investor Strategy

Bulls vs bears

Investor Strategy. February 2024. As market sentiment becomes bullish or bearish, it may present an opportunity to take the opposite stance. Reading the tea leaves…