Sign up here to receive the Market Ethos by email.

Market Insights

March 2022.

Russia’s invasion of Ukraine has sent shockwaves around the world, upending lives and disrupting industries and asset classes alike. To thwart Russia’s ability to fund its attack and to send a message to its political leaders wielding power, Western countries around the world have imposed increasingly stiff economic sanctions against the country. These sanctions have largely exiled Russia from global trade and finances and have left the rest of the world wondering what the potential longer-term implications of these sanctions will be on their lives. Commodity prices have dominated the investment headlines, and with inflation already at multi-decade highs, we start our discussion there.

Commodities: Ukraine and Russia’s influence

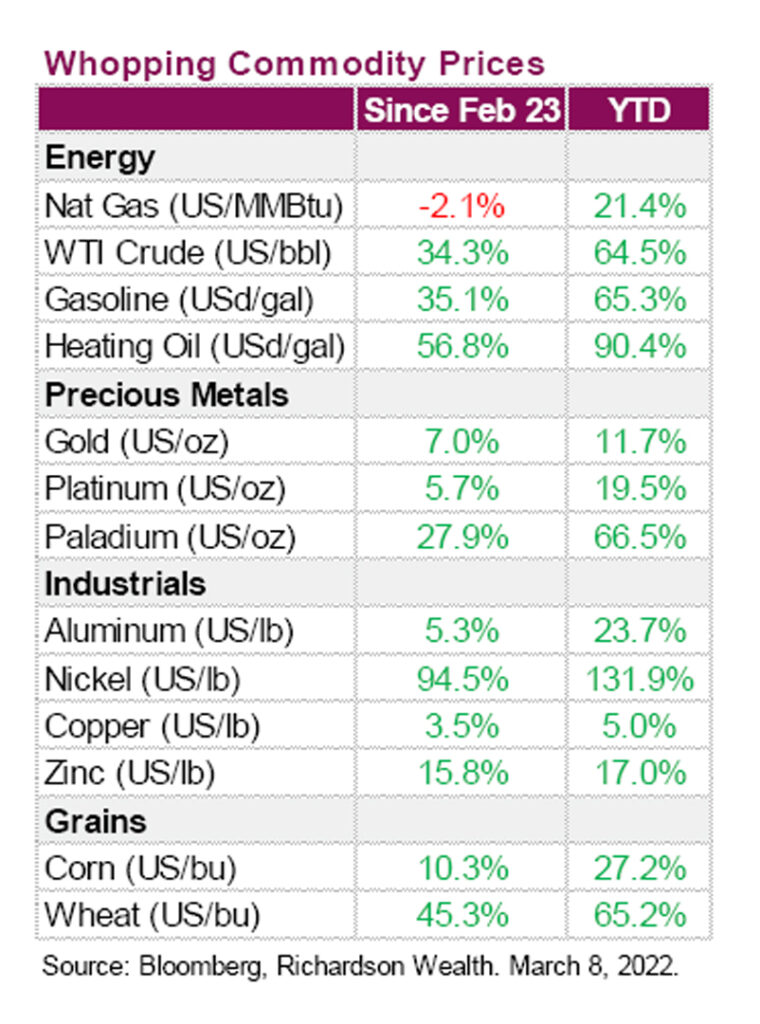

While Russia represents only 2% of global GDP, the country is a major oil and gas exporter. This makes any supply disruptions to these commodities more onerous to a system already reeling from the effects of pandemic-induced supply constraints matched with pent-up post pandemic demands. As several Western countries look to remove Russia f rom the global oil supply chain, prices have soared, putting further pressure on the commodity. Ukraine is also a major agricultural exporter of grain (including wheat) and vegetable oil (Ukraine is the top exporter of sunflower oil), however exports have stalled as customary trading routes have become more difficult to navigate. These delivery disruptions have further strained global food supply chains, exacerbating the inflation that began soon after economies reopened when surging demand was met with supply constraints and logistical challenges. These rising commodity prices have not only reverberated through the markets but also trickled down to the cost of living, contributing to rising inflation. To put the exposure into context, here are some commodity statistics:

- Russia supplies approximately 10% of global oil supplies and 40% of Europe’s gas

- Russia is sixth-largest coal producer accounting for more than 5% of global production

- United Company RUSAL (HQ in Russia) produced 3.8 million tonnes of aluminum in 2021, about 6% of the estimated world production

- Russian company Nornickel is the world’s top producer of refined nickel, about 7% of global mine production

- Nornickel is also the world’s largest producer of palladium and major producer of platinum, contributing to Russia’s 25-30% production of global palladium and platinum. Palladium is key for automakers for catalytic converters in exhaust systems to reduce emissions

- Russia is the world’s third-largest producer of gold and accounts for about 10% of global mine production

- Russia is a major producer of fertilizer components potash, phosphate and nitrogen and is 13% of the global total

- Russia and Ukraine are both major wheat suppliers, accounting for a combined 29% of global exports, the majority of which go through ports in the Black Sea

- Ukraine is one of the world’s top four corn (maize) exporters. Ukraine and Russia account for about 80% of global exports of sunflower oil.

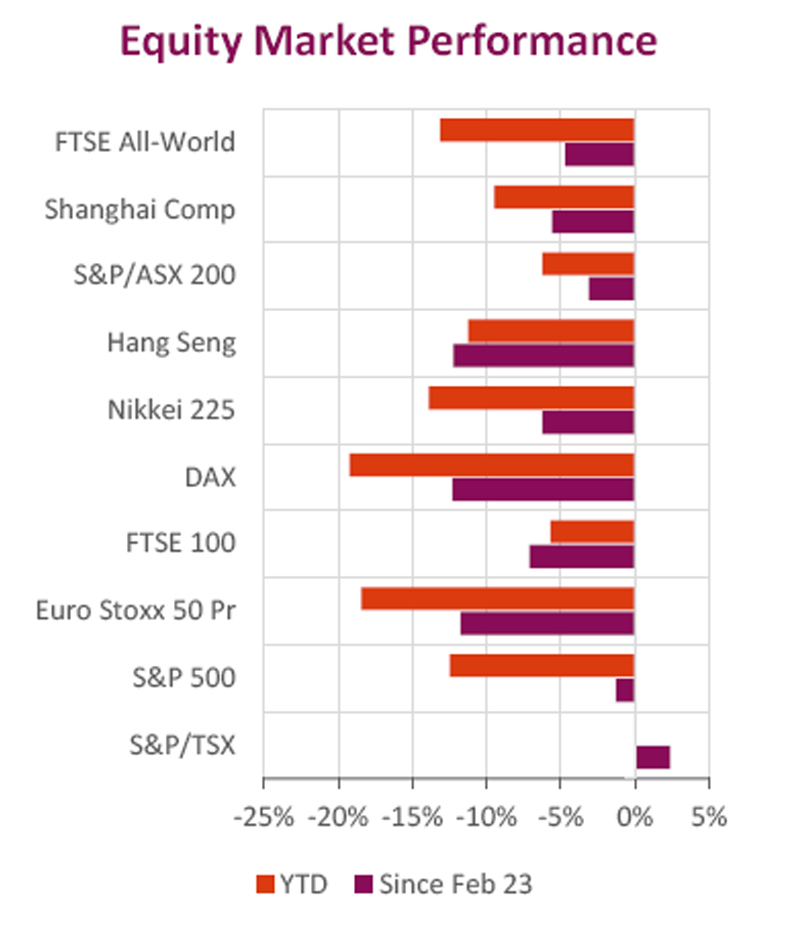

Equity markets: Canada vs. the world

Equity markets have oscillated since the onset of the war, sometimes posting intraday losses, only to recover by market close. Canada, with its heavy bias to resources, has fared well and is one of the best-performing markets since Feb 23. In the U.S., where technology and growth stocks dominate, the outcome has not been as favourable, with “risk-off” sentiment pushing the S&P 500 down to correction territory (-10% or more from peak) and the Nasdaq down to bear market territory (- 20% or more f rom peak). The main European equities benchmark has corrected from its January record high, amid fears that sanctions targeting Russia will exacerbate inflationary pressures and derail the region’s economic recovery. Investors are waiting for a European Central Bank meeting for more clarity on the wind down of stimulus measures, while a summit of the continent’s leaders this week may offer clues on potential fiscal support tools to cushion the economic fallout from the war. The market remains extremely headline-driven, swinging from hope of European fiscal support to despair about lack of alternatives of buying oil and gas from Russia.

Bond markets: Central banks proceed with caution

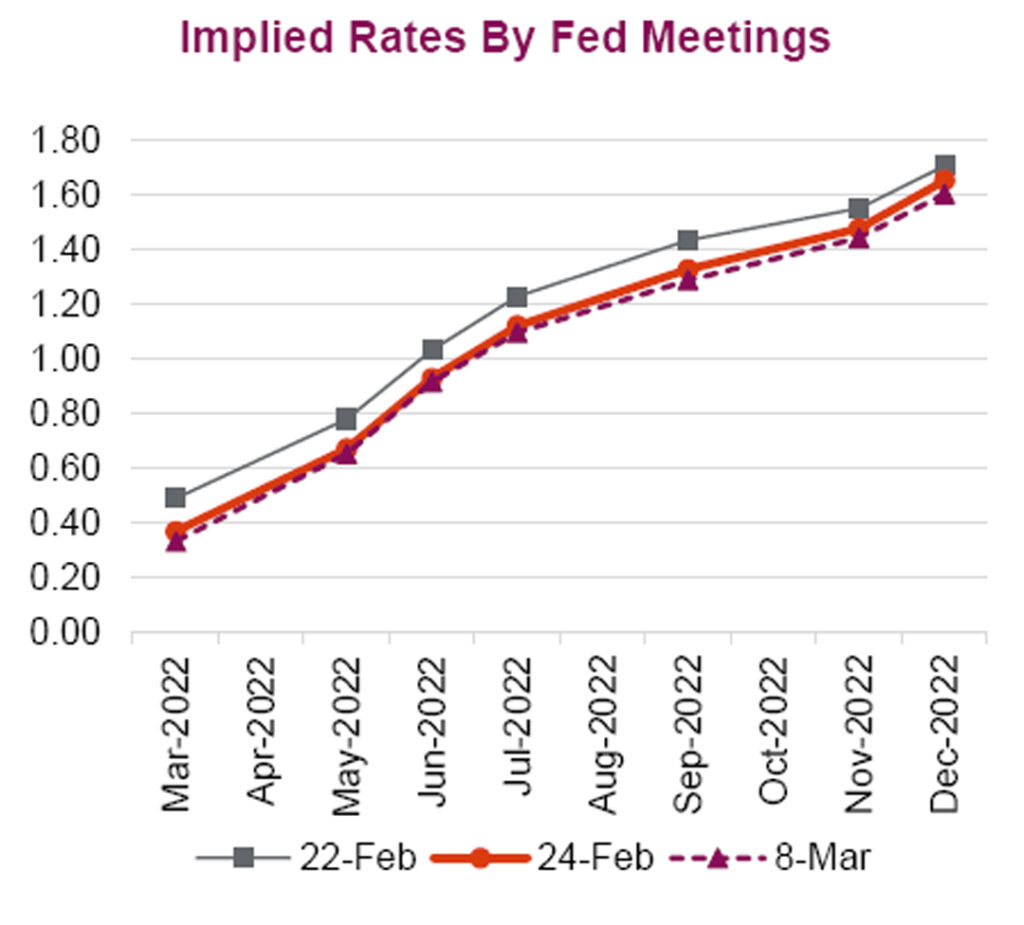

Meanwhile central banks are now in a difficult position of balancing policy with potentially weaker economic growth and higher inflation. Prior to Russia’s attack, North American futures markets predicted the central banks raising rates five to six times. Following the attack, these expectations have come down a notch. Last week the Bank of Canada started what is expected to be a series of interest-rate hikes as it tries to contain inflation. Policymakers increased the benchmark overnight rate by a quarter percentage point to 0.5% which was the widely expected move. In the U.S., the Federal Reserve (the Fed) is also on track to raise interest rates this month. However, Fed Chair Jerome Powell did say that the Russian invasion of Ukraine will require the central bank to be careful in how it conducts policy due to the uncertainty the war has caused. Powell said that he would be recommending a 0.25% increase at the central bank’s next meeting but did not rule out a 0.50% increase at a future meeting if pricing pressures don’t ease.

Summary

We can predict few things in the markets with certainty let alone a full-scale attack on a sovereign nation and its impact on f inancial markets. However, increased volatility due to macro-economic and geopolitical events is not uncharted territory as it was only two years ago that the onset of Covid triggered a pandemic-induced recession which resulted in the fastest market sell-off ever recorded (of at least 30%). For investors, while exogenous events like these cannot be anticipated, having a resilient portfolio well-diversified across asset-classes, regions, and style should help the portfolio endure extreme bouts of market volatility and allow for opportunistic shifts to take advantage of market dislocations. Following Russia’s attack, global growth forecasts for the year have moderated and with no imminent resolution to the conflict in sight, we anticipate market volatility to continue. With that said, the situation is changing rapidly but during these uncertain times, it is important to remain focused on longer-term investment goals with an eye on rebalancing should the opportunity arise. Please remain connected through our website for current insights on market strategy and portfolio construction.

Source: Charts are sourced to Bloomberg L.P., and Richardson Wealth unless otherwise noted.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by the author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Richardson Wealth does not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publicationor research report from Richardson Wealth, and is not to be used as a solicitation in any jurisdiction.

This document is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.