Market Ethos

25 May 2026

A tale of two consumers

Sign up here to receive the Market Ethos by email.

Most investors have likely come across the concept of the K-shaped economy — our industry does love to put letter shapes on things. In this case, the K denotes a split in the U.S. consumer, with some doing REALLY well (the upward-sloped arm of the K) and some doing REALLY poorly (the downward-sloping arm of the K). Folks who own assets, stocks, property, businesses, are doing fabulously well. With markets near all-time highs and up a lot, the Bloomberg World Equity index has annualized 21% over the past three years. This has a tremendous wealth effect on consumers, but mostly just those with enough net worth invested in assets.

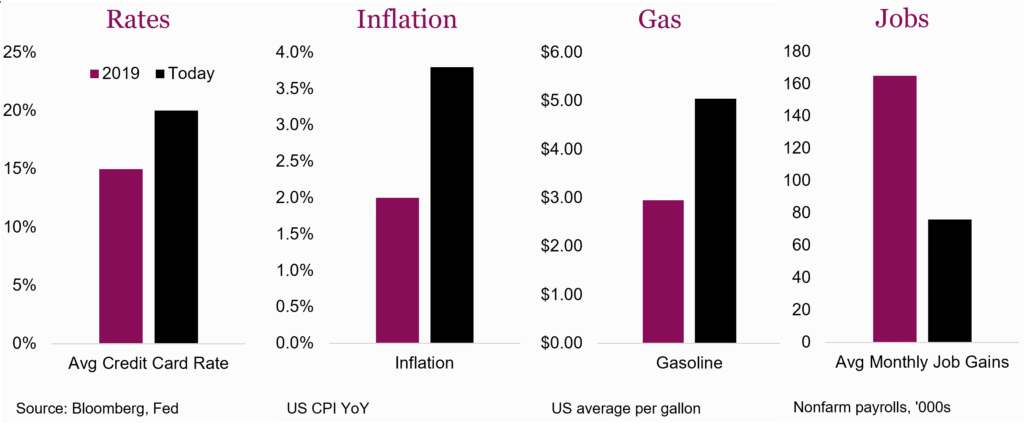

On the flip side, those who don’t own a lot of assets are dealing with wages that are growing but barely keeping up with inflation. Inflation, still high, is a tax on consumption so anyone who spends more on consumables is impacted more. If you are a big saver, its impact is not as strong. Add to this gasoline prices of $5/gal, up over 50% since the start of the year (U.S. average). Interest costs remain high and show little sign of coming down, given the recent uptick in inflation. And some would argue that policy in the U.S. over the last while has been skewed to benefit the wealthy versus the less wealthy.

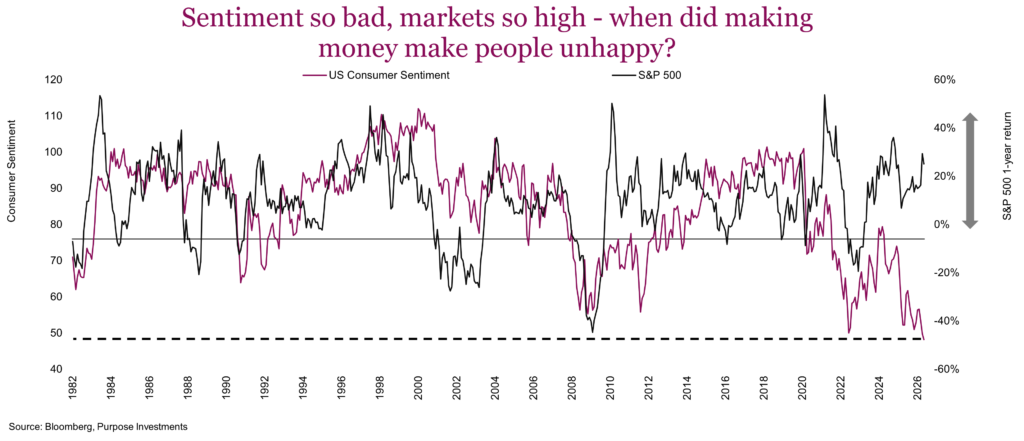

The K-shaped mood is certainly evident in consumer sentiment surveys. The University of Michigan Consumer Sentiment Index (chart above) asks consumers about several things with the attempt to garner their willingness to buy stuff. It covers aspects like personal finances, general business conditions, what the markets are doing and prices. In May, it reached its lowest level since the survey inception in the late 1970s!! So, based on this survey at least, consumers are more in the dumps than during COVID or the financial crisis or the high inflation period in the late 1970s / early 80s. Is it really that bad?

Historically, changing consumer sentiment has correlated with moves in the stock market. It’s hard to say whether a happier spendy consumer makes the stock market go up, or if the market going up makes consumers happy. Bit of a chicken and egg issue. Today though, markets are at new highs and the consumer is catatonic. This is very odd but there are some factors contributing to this divergence:

- Surveys – The efficacy of surveys has been on the decline over the past few years. Polls fall into this grouping as well. It seems respondents often answer one way and behave differently. And the response is more often negative, even if many consumers are clearly still spending.

- Composition – The market is asset weighted; in other words, the attitude of the wealthy has a MUCH bigger market impact than the attitude of the not so wealthy. The S&P is certainly not an equal democracy. However, it may be more #1 because if you break down the consumer sentiment by income, the wealthy are in a marginally better mood than the lower income cohorts, but not by much. Maybe everyone is grumpy.

Survey nuances aside, folks are not happy or confident. Inflation, gas and interest rates are a tough combo right now. Plus, job growth has been very lackluster. There are a lot of moving parts in labour from participation rates, demographics, immigration and maybe AI. This does appear to be making the unemployment trend higher at the ‘new entrant’ cohort, while remaining low and stable at more tenured employees. This may also be contributing to the recent uptick in productivity, maybe AI or less new entrants. Sorry new entrants, despite your eagerness you just aren’t productive for some time.

Fortunately, the upper arm of the K simply matters much more —not just for the stock markets, but for the economy. So, while the lower arm of the K is struggling, the upper arm is spending, travelling, doing enough to keep TOTAL consumer spending growing. To be fair, the economy has always been K shaped, this isn’t new. Perhaps the spread is just getting wider.

Watch the wealthy

With lower income cohorts struggling and higher income cohorts doing well, we should keep an eye on the spending habits of the higher income folks. Because, while not fair, they are the ones that matter more for the overall economy. So how do we gauge their mood or spending habits?

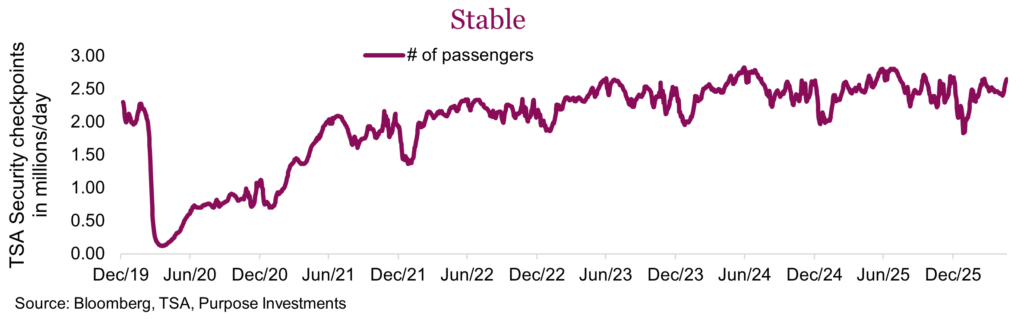

We have come up with four metrics: two on services and two on goods. Travel is also a discretionary component of spending and tilted towards higher income consumers. Of course, business travel skews this data. Pricing is also a challenge, as we can see big upswings in airfare spending recently — but is this simply the result of rising ticket prices due to higher oil prices? So, we will opt to track number of passengers moving through TSA security checkpoints.

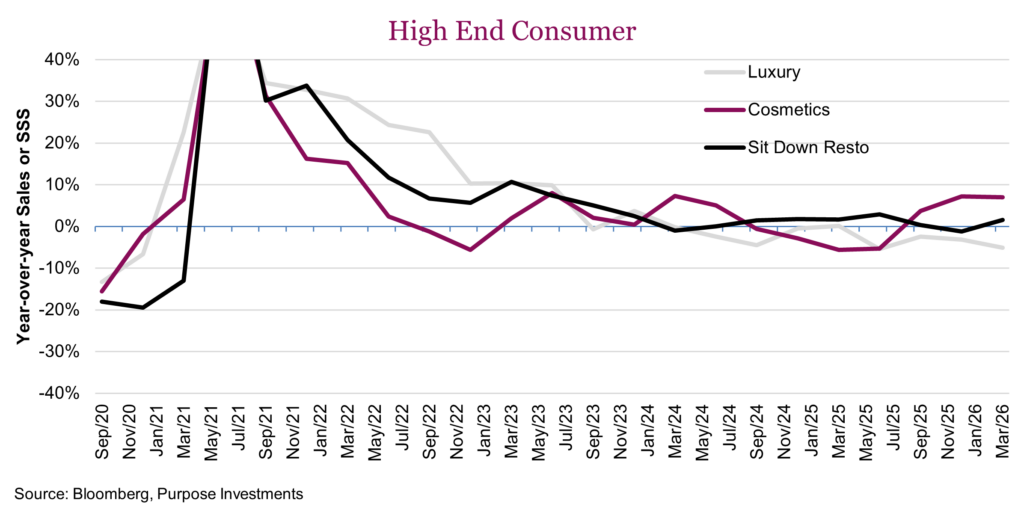

Most high-end restaurants are private, so it’s kind of hard to get a feel for volumes. However, we believe the trend in sit-down restaurants may provide some insight. Perhaps more across the income cohorts, the decision to eat out versus eat at home or quick serve is certainly a discretionary spending decision influenced by your personal financial situation. After creating a composite of 11 publicly traded sit-down restaurant chains, we compiled the average same-store sales over time.

The goods-related spending indicators are cosmetics and luxury. While we can debate whether skin care is discretionary or not, it is a category dominated by higher income cohorts and historically has proven very cyclical. Measuring luxury spending involves mostly European companies. We created a composite of seven global luxury brand companies covering a diverse range from purses, fashion to watches.

Broadly speaking, the trends are decent based on these metrics. Not improving but not rolling over either. We will take this to mean the upper arm of the K is still spending.

Final thoughts

The consumer drives the global economy. In fact, the U.S. consumer alone accounts for about 18% of the global economy. No denying the lower income U.S. consumer is in a tough spot, but the higher end continues to spend, hence the K-shaped economy. But don’t fret the K at this point; we would only become worried if evidence arose to show the wealthy are starting to dial back. If, or when, that happens, look out because there is not much support further down the income spectrum.