Market Ethos

April 8, 2024

Dividend disruption

Sign up here to receive the Market Ethos by email.

Dividend investing is supposed to be easy. Find quality companies with a long track record of paying or even increasing their dividends, buy some shares, collect your regular tax-advantaged payments over time and watch the share price go higher. In a strong bull market, dividend companies don’t rise as much, but they have better stability in down markets as most are lower beta than the overall market. Well, over the past year the TSX is up about 13% while the Dow Jones Canada Select Dividend Index (a good proxy for dividend investing) is up a mere 3%. Trailing in an upmarket is fine, but not by that much.

The DJ Select Dividend index was created in the late 1990s and this is only the fifth time that it has lagged the broader TSX by more than 10% on a trailing one-year basis. Interestingly, most of the previous occurrences coincided with brief periods when a non-bank became the largest weight in the TSX. In the late 1990s it was Nortel, in 2007 it was Encana, Potash, and Blackberry. The 10% threshold was almost reached in 2015 when Valeant become the biggest company in the TSX. And in 2019, it was Shopify.

This makes this recent bout of underperformance of dividends versus the broader TSX unique, as the biggest stocks in the TSX remain dividend payers, including Royal Bank and TD Bank. Plus, the banks have been doing ok. It is the other dividend payers that have dropped considerably that are dragging down the dividend space. Communication Services (aka Telcos) are down 24% over the past year and Utilities down 15%; two areas that are fertile with dividend-paying companies.

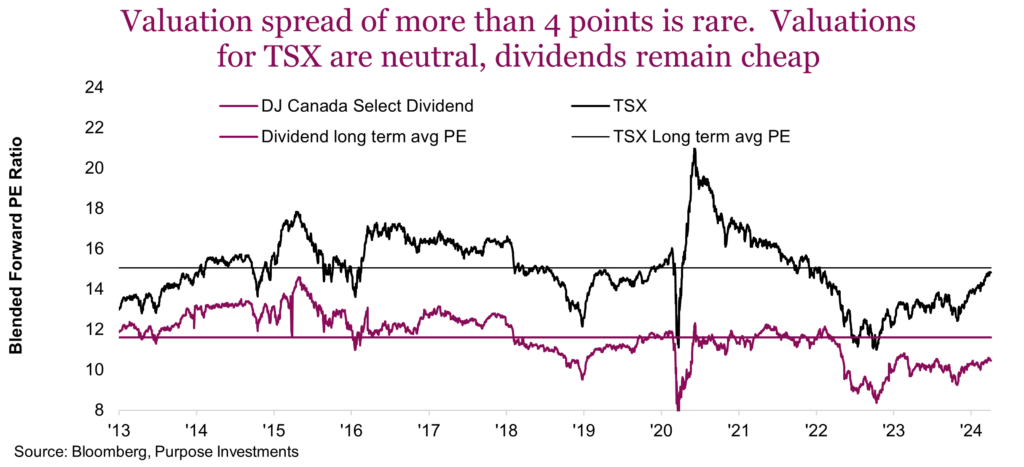

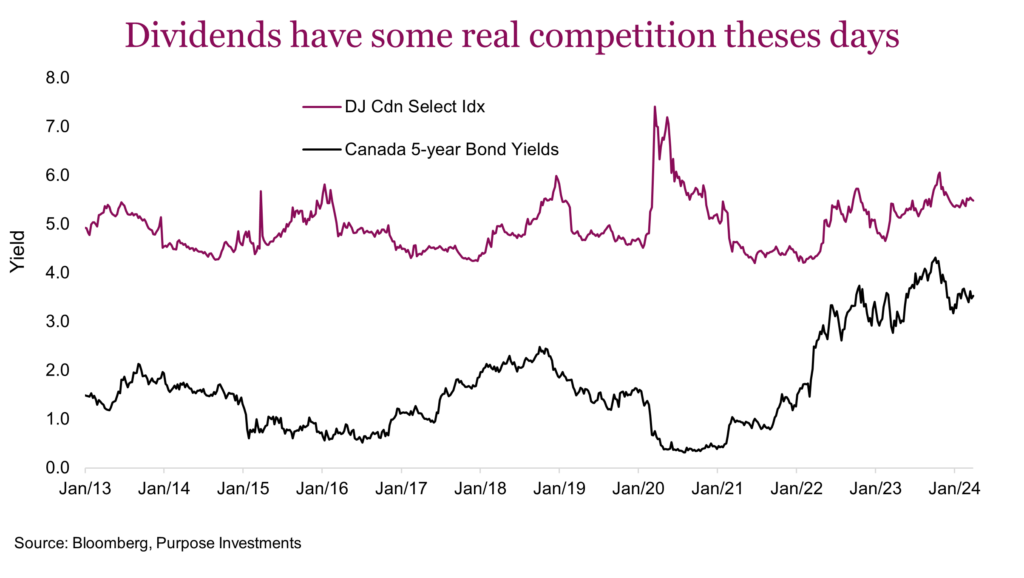

This has the valuations in the overall dividend space at roughly 10.5x forward earnings estimates, while the broader TSX is closer to 15x. That is a historically wide spread. It was wider in 2020 but that is because the TSX’s earnings almost went to zero during pandemic – not because of a higher index price. While dividends may be cheap versus the TSX, the real crux of the weakness stems more from relative yields. Bond yields moved higher in 2022 and have been maintaining at historically high levels compared to the past decade. This is a clear competitive investment for those looking for yield.

One could even argue that dividend yields need to increase even more to remain competitive against yields available in the bond market. This isn’t an apples to apples comparison. Bonds benefit from greater stability as a true risk-off asset class. Dividends benefit from a history of growing the dividend rate over time, and some appealing tax treatment. Plus the stock price could go higher while bonds mature at 100. But dividends can also get cut and companies can even go bankrupt. We will assume the 5-year government of Canada bond has a low default risk.

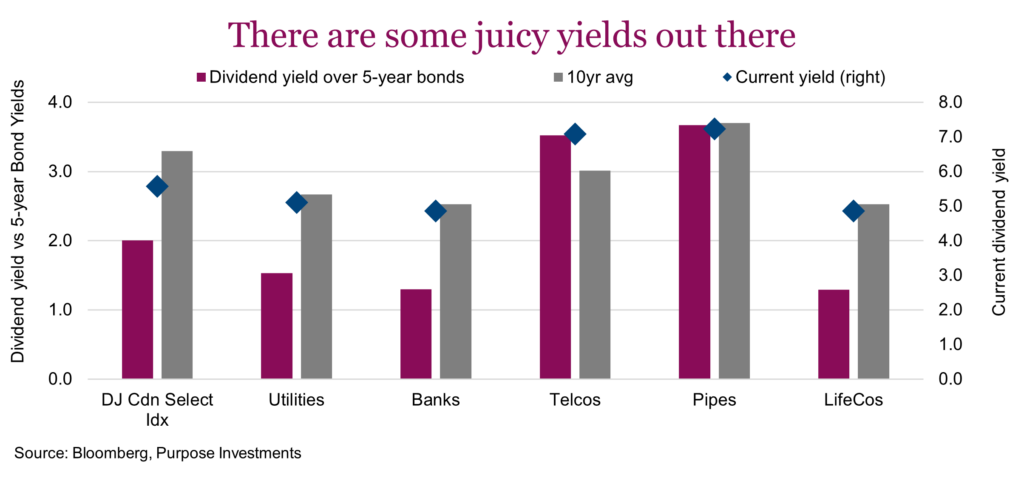

Yet while the overall DJ Cdn Select Index dividend yield may not look overly enticing compared to bond yields (above chart), digging into specific sectors does show a different picture. The chart below shows the current dividend yield across various dividend heavy sectors compared to 5-year government of Canada bond yields. It also shows the 10-year average spread and the nominal dividend yield. The overall dividend space may not be hugely enticing on a relative yield basis, but telcos and pipes sure are, with each yielding about 7%.

Final thoughts

The dividend space has clearly become challenging over the past year, given higher bond yields. But it isn’t just bond yields. The increased popularity of other sources of yield has certainly risen over the past number of years, from the structured notes space to covered call strategies being applied to just about anything with a live option chain. The search for yield has never had so many choices. So, what could turn this tide and help the performance of dividend payers close that gap with the broader market? Not sure, maybe a broad market sell-off that cools the more aggressive risk-on behaviour. Maybe central bank rate cuts or lower bond yields. Or maybe just the realization that buying operating companies with decently safe dividends in the 5-7% range and attractive valuations offers a good risk/reward combination and a decent income stream as you wait out this dividend depression.