Market Ethos

27 April 2026

Market Q&A

Sign up here to receive the Market Ethos by email.

The missile and drone launches have quieted, the Strait of Hormuz isn’t really open, unless you want to be boarded by either Iranians or Americans, the talks are on or off depending on which headline you read. Fortunately, Mr. Market has largely moved on, with most indices making fresh new highs. Of course, this could change at any moment, but we will take this relative pause as an opportunity to switch topics for this Ethos: what are the most recurring questions that have been on the mind of investors these days?

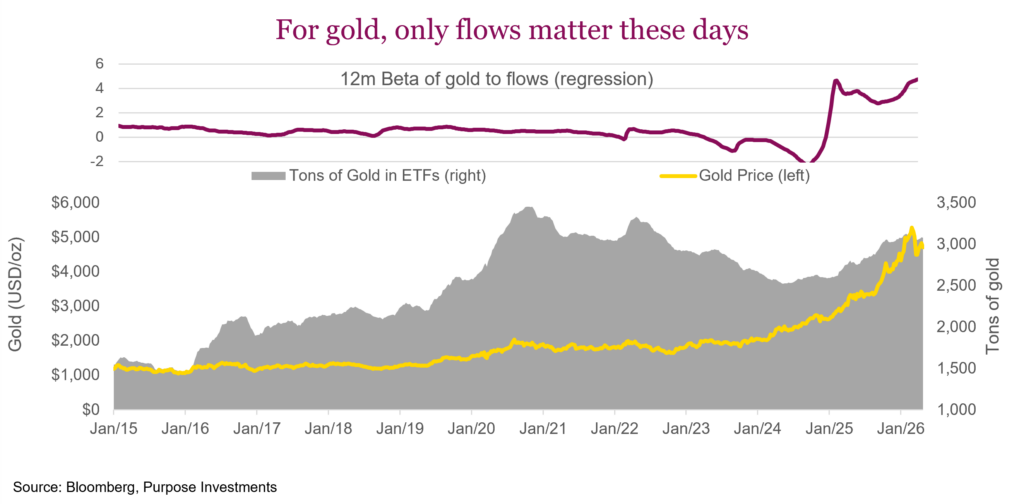

What is going on with gold?

Gold has a very long and successful history of providing crisis alpha, a stabilizer for portfolios when the world goes wonky. If you were asked what gold would do if hostilities broke out between the U.S. and Iran, spiking geopolitical risk higher, most would be in the camp that gold should go up in price. Surprisingly, gold is down -12% since hostilities began and, at one point, was down nearly -18%. Meanwhile gold miners, as measured by the XGD ETF, are down -18%.

The challenge for gold during this conflict is twofold: it had already run really hard to the upside and it was not all about flow momentum. Investors are well aware gold has experienced some very outsized gains during the past couple of years. Rising +27% in 2024 and +65% in 2025, plus rising +23% through the end of February before the conflict began. And during this strong bull run, there really wasn’t any great crisis.

The central bank diversifying their reserves, mildly bearish sentiment towards the U.S. dollar or other factors probably got this bull run going. But like anything, once the performance started shining, the flood gates opened with more investors piling in. How many investors started asking – ‘do I have any gold in my portfolio?’ As a result, since mid-2025, gold has moved in lockstep with financial flows. With flows as the dominant price driver, rising or falling geopolitical risk simply hasn’t been as strong an influence on the price as it usually is. Nor are real yields, the U.S. dollar or other historical gold price influencing factors.

When the conflict started, investors sold some gold ETFs, dropping holdings from 3,139 tons to 3,050 by the end of March. That is when holdings bottomed and so did the price of gold. At some point, other factors will rise back up in prominence for driving gold, but for now it’s all flows.

That isn’t a bad thing. Trust in the system is certainly not high for too many reasons to list, and investors have returned to gold. That could easily continue and have a big influence on bullion prices, but it will cut both ways. Gold, is not so much a provider of crisis alpha these days, more just pure alpha (by the way we still own gold).

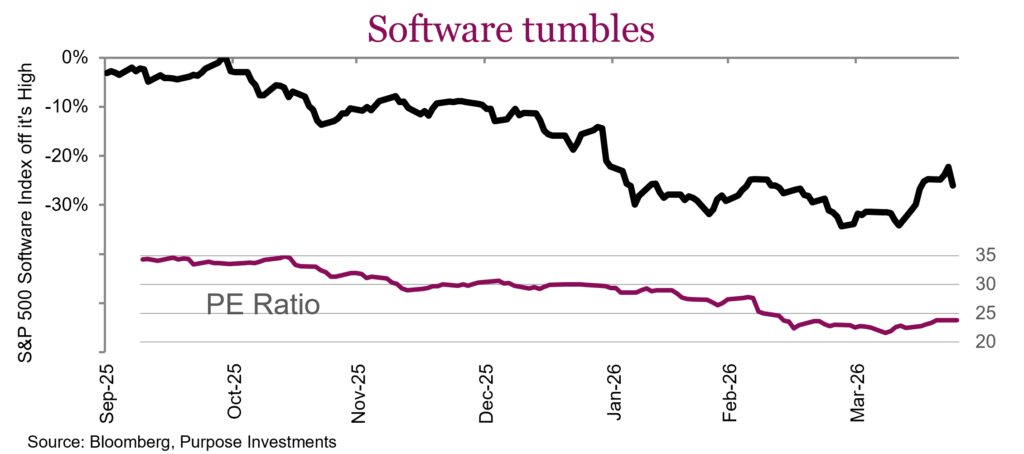

AI disruption / software selloff – opportunity or value trap?

Technology has always moved pretty fast and given the dramatic proliferation of artificial intelligence (AI) tools, it is moving even faster these days. Up until last fall, it was broad-based excitement, anything AI-related news and share prices of any company simply jumped higher. This started to change in late 2025 as investors started first to question the returns on these massive capex spending plans by the hyperscalers. And in 2026 it changed again as investors started worrying about the impact of AI on various industries, namely if those existing business models will be disrupted.

While this disruption fear has popped up in many industries from law, credit rating, exchanges and trucking, it has been most acute in software. This pushed the S&P 500 software index down more than -30% in a few months while the broader market has generally moved higher. The price-to-earnings multiple for software contracted from nosebleed levels of 35x down to the low 20x, roughly in line with the broader market. Prices have imploded while earnings estimates for 2026 and 2027 have continued to rise during this selloff.

Markets often overreact in the short term and under react to long-term changes. This does appear to be the short-term overreaction phase. Over the past 30+ years, there are very few occasions when software traded at or below the market multiple. We believe this is overdone but certainly acknowledge that the narrative around software is very negative, and this is a narrative-driven market.

Narrative-driven market?

Markets have always had a storytelling aspect, perhaps because most content created in the investment world is really trying to put what has already happened into context. However, more recently the speed of narratives, and the impact, has become faster and larger.

There are many contributing factors to this trend. It has been a long time since we have had a real bear market, so investor fear is minimal. News headlines have increasingly become more polarized at one end of the spectrum or the other. A good example is AI and if it will either create a limitless society or destroy the world. One reason news has become more extreme is to get attention of the algorithms it has to capture attention. This can easily amplify a narrative to drive investor behaviour.

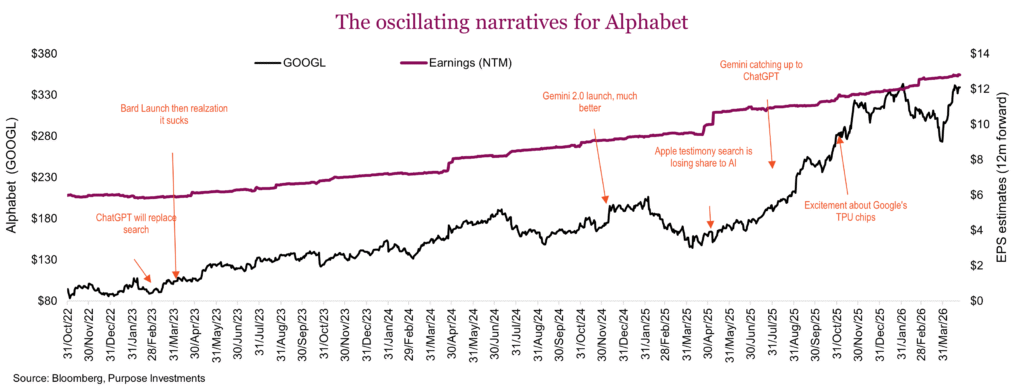

Borrowing the example from a Morgan Stanley conference, the chart below is the oscillating narratives around Alphabet (Google). Periods of angst as the market narrative that AI will replace search engines make the rounds. Countered by AI product launches from the poorly received Bard to the well-received Gemini 2.0. Then, excitement that Gemini was closing the market share gap with ChatGPT, followed by the excitement that Alphabet was starting to sell their TPU chips to other providers. Meanwhile, earnings estimates continue to move in a steady line up and to the right. Earnings matter in the long term, narratives drive the short term.

We will be diving deeper into this topic in future Ethos, as we believe the dynamics of the market have changed. In the meantime, just keep in mind narratives have become more powerful than before while fundamentals are being somewhat pushed to the back.