Market Ethos

20 April 2026

Hiding in plain sight

Sign up here to receive the Market Ethos by email.

Despite the recent roller coaster in equity markets, investors should be happy with returns so far this year. Especially Canadians, with the S&P/TSX Composite now up over 8% year to date, and Canadian energy having its best quarter in a decade. At times, sticking with a winning trade is the right thing to do. It is the basis of momentum, after all. However, this isn’t always the case, especially when it comes to cyclicals. Your gut may not be screaming it’s time to trim energy, but that’s exactly why you should be strongly considering it. The Hormuz blockade is real. The supply crisis is real. We don’t dispute the severity, but the big moves in the energy market have already priced in much of this risk, producing something more dangerous for investor portfolios. Just like the classic Tom Clancy thriller Clear and Present Danger, the hero’s problem isn’t the enemy, it’s that his own side doesn’t realize how exposed they are. Canadian equity portfolios face a similar plot twist.

Just as we’re sending this Ethos prepared to publish, the Strait of Hormuz has reopened and closed somewhat, and oil prices have dropped -10% and then jumped 5% before and after the weekend. What follows was written before those headlines, but the thesis holds. If anything, this energy market move is proof of concept.

The accidental bull

We entered the year constructive on equity markets, but after such a strong 2025, we viewed the odds of Canadian markets delivering a similarly strong start to 2026 as slim. With high sector concentration, there are only so many levers the market must pull to generate genuine strength: financials, materials and energy. Back in January, we advocated for maintaining energy exposure during the Venezuelan selloff despite fears of a supply glut in the first half of the year. That call was right, though for entirely the wrong reasons.

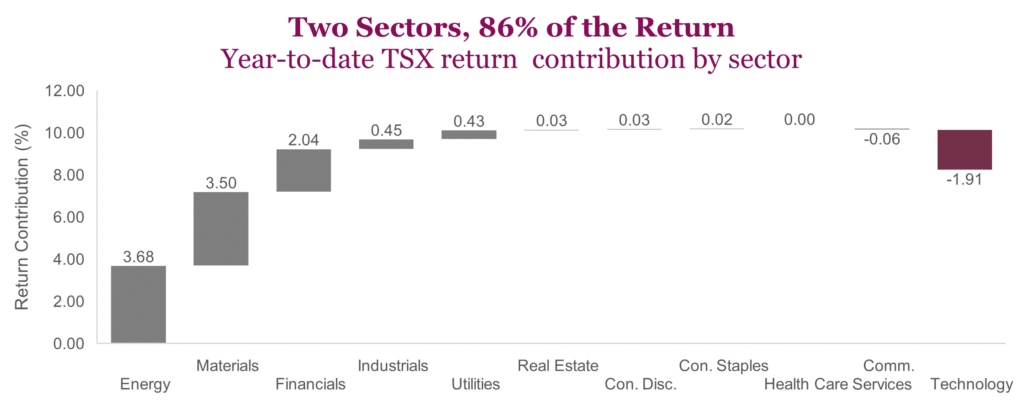

Year-to-date, the S&P/TSX Composite is up about 8.3%. The chart below is a sobering visual. The TSX isn’t a diversified index right now, it’s been a two-sector trade. Energy (45%) and materials (43%) account for roughly 87% of the entire TSX year-to-date return. Everything else is a rounding error, besides the drag of technology. Considering how no one would have predicted energy’s dominance this year, we’d classify the Canadian market as the accidental bull.

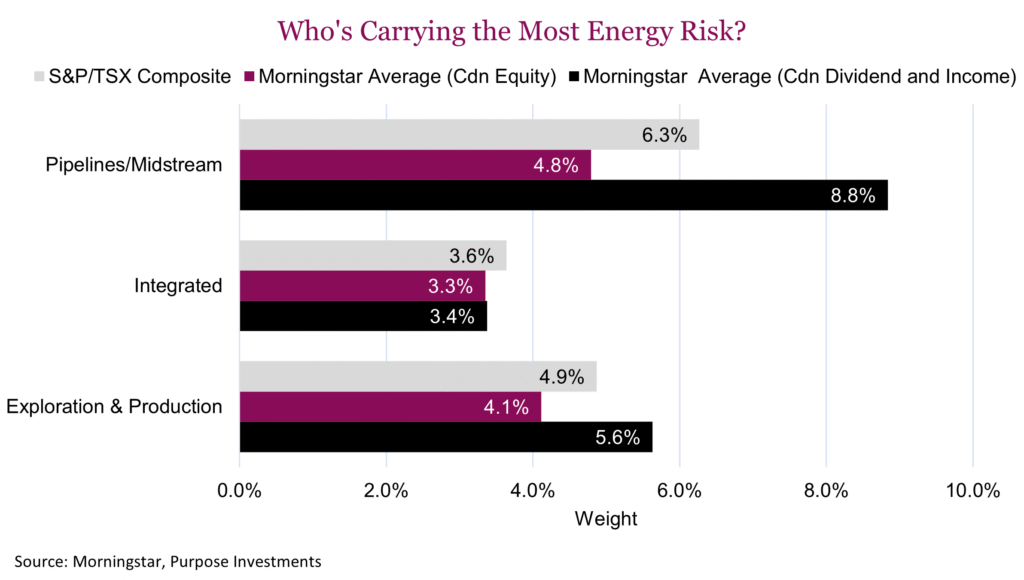

During bull markets, rebalancing is one of those boring exercises that doesn’t really feel like it’s going to generate real returns. But after such strong performance, the energy weight in the TSX has risen to levels that demand attention. Looking at E&Ps, integrateds and pipelines only, the benchmark weight sits at 15.2%. Pipelines and midstream remain the biggest single sub-sector weight, while higher-beta producers now account for over half the sector.

The chart below breaks out energy weights by sub-sector across two popular Morningstar categories and the TSX. Canadian dividend and income funds average 18% energy exposure, with many of the largest funds and ETFs in the category carrying upwards of 30%. Now most of this exposure is in the pipelines, but they still carry a higher weight in E&Ps than the TSX. Canadian equity funds on average hold just 12.7%, well less than the TSX which sits at just over 15% total.

Here’s where it gets uncomfortable. For many Canadians in or approaching retirement, portfolios tilt heavily toward dividend and income mandates. These are the clients who are most risk-averse, yet they likely carry the heaviest energy weight. The clients who can least afford a sharp retrace have the most exposure to one.

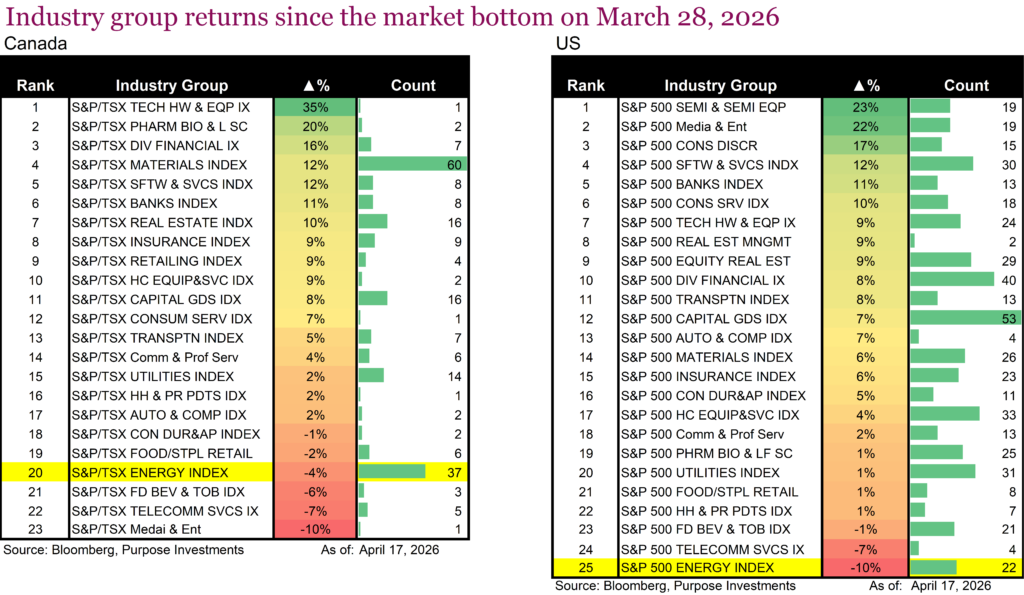

When a single sector dominates returns this completely, the risk profile has changed. Cyclicals are called cyclical for a reason. There are boom times, and these are followed by periods of leaner returns. We’re already seeing this play out on both sides of the border. Since the market bottomed on March 28, energy has been among the worst performing sectors in Canada at -4%. In the U.S. the pattern is even starker, with the S&P 500 Energy Index dead last at -10%. Meanwhile many other sectors are seeing terrific strength. In Canada, tech hardware is up 35%, diversified financials are up 16% and the gold trade appears to back on with materials up 11%. In the U.S., tech is leading big time, followed by consumer stocks particularly those hit by high oil prices. The rotation is already underway. The question is whether as an investor you choose to actively participate or just watch.

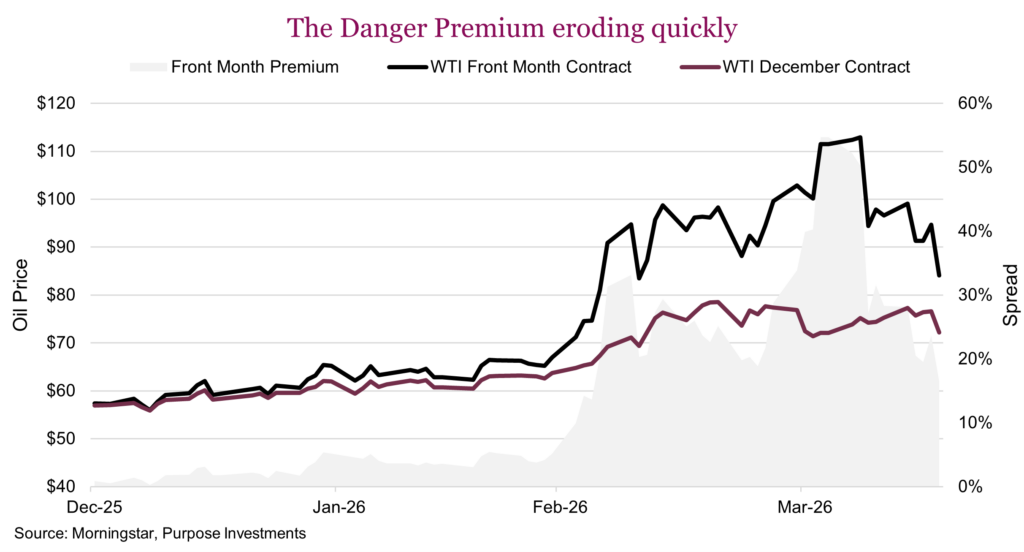

The danger premium

The equity market is already voting with its feet. The oil market is telling a similar story. The volatility in spot oil has baked a clear and present danger premium into futures markets. Spot WTI spiked from $60 to nearly $120 and has already pulled back 29%. Most of the violence was in front-month contracts. December futures barely flinched, rising modestly from $58 to $77. The front-month premium peaked at 55% on April 3 and collapsed to just 23% within weeks. Trimming while the premium is still elevated makes sense rather than waiting for the next compression.

Backwardation this extreme doesn’t last. It’s the market hoarding, not the market thinking. When the premium is driven by fear and logistics rather than a structural change in supply and demand, it compresses. The only question is when. The spot/futures gap is the market telling us two different stories. We’d rather be sellers of the panic version. Friday’s -10% drop on the Hormuz reopening is what that compression looks like in practice. The front month premium is still there, but is now well off the highs.

The active edge

As much as rebalancing is a practice in risk management, it’s also how you build the next leg of returns. We’ve been advocates of trimming energy over the past month, effectively monetizing the panic premium and redeploying capital into sectors where valuations have been compressed, cash flows are stable and earnings expectations are actually moving higher. Oil is already off its highs. The year-to-date gain has compressed from nearly 100% to roughly 60%. Portfolios that haven’t trimmed are giving back performance in real time.

Actively trimming and taking profits is a statement of discipline. We aren’t predicting when the Strait of Hormuz reopens, when gas prices will get back to $1.30 per litre, or when there will be peace in the Middle East. The range of outcomes is so wide and dependent on so many variables that holding elevated exposure at this point isn’t conviction, it’s complacency. The move that’s already happened in the futures curve is telling us that the danger premium baked into energy markets is already dissipating. From our vantage point, as well as the market’s, on-again off-again talks are enough to move on.

The danger was clear and present. The premium was there for the taking. This morning’s big move in energy markets won’t be the last. The danger premium will likely widen and compress again as headlines shift. The key is to be on the right side of that volatility, not hostage to it.