Sign up here to receive the Market Ethos by email.

Market Ethos

May 15, 2023.

Over the past few weeks, we would say the news has been tilted solidly towards the ‘good’ side. The world’s largest central bank (Fed) effectively announced the cessation of rate hikes, ending a fourteen-month journey that raised overnight rates from 0.25% to 5.25%.

Q1 earnings season is wrapping up, and it finished stronger than it began. With over 90% of companies having reported, 77% surprised to the upside, with an average magnitude of 6.5%. We have not seen that large of a surprise in a couple of years. Of course, you could be bearish and point out that Q1 earnings had been almost $60, and forecasts fell over the past few months to just over $50. So the surprises were against some rather low forecasts. Nonetheless, the earnings season finished well.

Inflation has improved. The US reported April CPI data that continued to show signs of improvement. It was the first year-over-year print below 5% in the past two years, at 4.9%.

Labour remains resilient in both Canada and the US. Of course, this is a double-edged sword as too much good news would be inflationary, but a strong report for both Canada and the US, including solid gains in higher-paying jobs, is good news for the economy. At least showing recession risk as not being imminent.

Sure, there is some not-so-good news as well. Consumer confidence moved lower, the debt ceiling remains top of mind, and the US regional bank stresses remain. But taken as a whole, the news of the past couple of weeks has been good. One would expect this preponderance of good news to lift the market higher, but that hasn’t happened. The daily gyrations have been up and down, but overall, markets are down slightly in May so far. The S&P and TSX are both off a minor 1%.

When good news fails to lift markets higher, Mr. Market is saying something and we should all listen. In the near term, the path of least resistance may be to the downside.

Debt ceiling

We have a history of rarely weighing in on politics for a few reasons. One, we believe the economy is usually a bigger deal than any change in policy. Of course, there are exceptions to this, but it is a good general rule. Secondly, good luck trying to guess the likely path of policy decisions, as what should be done for the markets/economy is often confounded by ideological views. Thirdly, even if you ‘guess’ right as to what the policy, announcement or outcome may be, how the market reacts is equally challenging and often surprising. Take the debt ceiling debate. We feel confident it will be raised, but how we get there is a guess. Maybe it will be resolved quickly without any disruption. That is our base case, remembering the last time this became a tenacious topic over a decade ago. The government started to shut down, which impacted people who voted, resulting in a drop in support for the party viewed as the blocker. Neither party likes to lose votes.

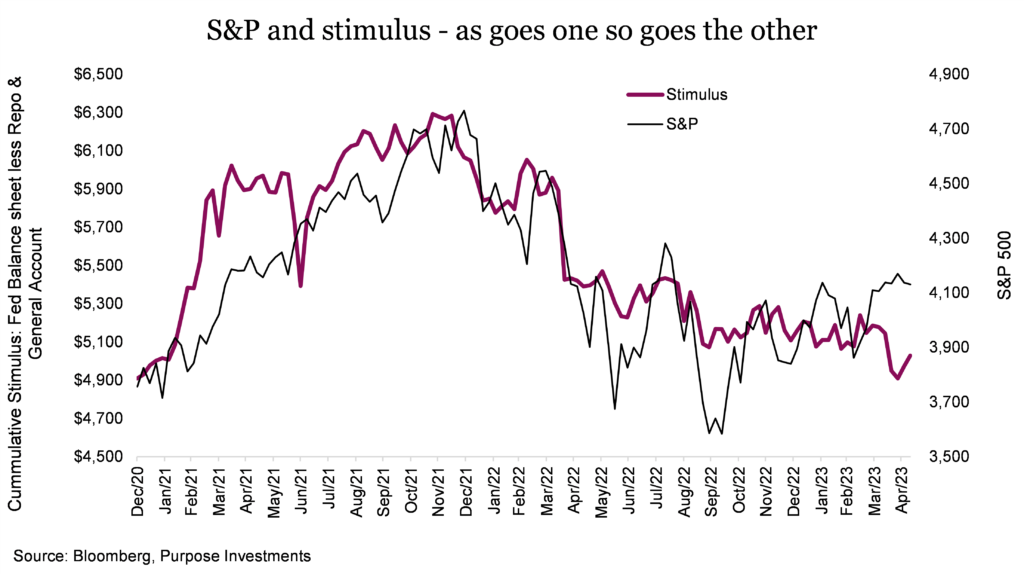

A debt ceiling resolution would certainly be good news, and perhaps markets would react positively. BUT, that may be short-lived. The markets for much of the past few years have been very sensitive to the amount of stimulus. During periods of more stimulus, equity markets have advanced, and during periods of dwindling stimulus, markets have fallen. The chart above highlights this relationship. While not a perfect fit, directionally, it is very strong.

Stimulus is a combination of measurements that really center around the Federal Reserve’s balance sheet. Most are aware of the expansion of Fed assets as a quantitative stimulus tool at their disposal. The stimulus we track includes this and also incorporates the Repo market and General Account. The Repo market is a kind of parking spot for excess liquidity for banks and other institutions. Effectively it is money being diverted out of the economy/markets and being re-deposited with central banks. So the size of the Repo market is subtracted from the total stimulus.

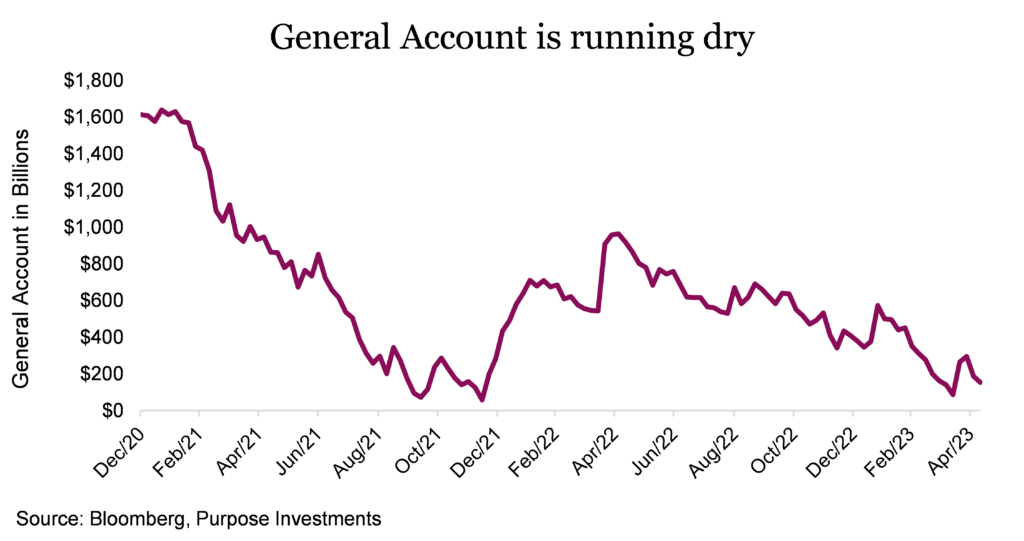

The interesting component of the debt ceiling is the General Account. Think of this as the government’s chequing account. If they write cheques to consumers or businesses or for projects, this is stimulus back into the economy, and the account goes down. That is why the account is subtracted from the stimulus. So if the account gets smaller, that is stimulus. And it sure has gotten smaller.

With the debt ceiling looming, the General Account has been bled almost dry. So what will happen when the debt ceiling is raised? Well, the government will likely replenish this account by issuing Treasuries. As investors buy those Treasuries, money/liquidity/stimulus will be removed from the markets. So that aqua line in the first chart will likely move lower. And what about the other assets on the Fed’s balance sheet? Well, the Fed has continued to reduce their asset holdings, combining for potentially an even bigger drop in the total stimulus.

This is a simplified lens into central bank balance sheets regarding the ebb and flow of stimulus. And we have omitted the stimulus provided to banks via Primary Credit Loans and the Bank Term Funding Program. Both of which exploded in size as US regional banks rushed to replace fleeing deposits. Technically this is a stimulus not captured in our framework. But that is because we do not believe banks using these programs are rushing out to inject that money into the economy via loans or investments. Most banks are becoming increasingly tight on lending, given the uncertainty of their deposit base.

Final thoughts A resolution to the debt ceiling will be good news since no resolution is really bad news. But it may not prove to be a lasting panacea for the markets as it could trigger less stimulus in the weeks or months afterwards. So once again, even this good news may do little to lift markets higher.

Sign up here to receive the Market Ethos by email.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Richardson Wealth Limited for information purposes only.

*This report is authored by Derek Benedet, CMT a Portfolio Manager at Purpose Investments Inc. Effective September 1, 2021, Derek Benedet has transitioned to Purpose Investments Inc.

Disclaimers

Richardson Wealth Limited

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Richardson Wealth warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Richardson Wealth or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.

Richardson Wealth Limited, Member Canadian Investor Protection Fund.

Richardson Wealth is a trademark of James Richardson & Sons, Limited used under license.